Switching your Medicare Part D plan might feel overwhelming, but it doesn’t have to be. Every year, thousands of people change plans to lower their costs, get better coverage, or access a wider range of prescriptions. With the right steps, you can switch without gaps or penalties.

This guide will walk you through everything you need to know, when you can switch, how to do it, and how Prime Life Financial makes it easier.

Why People Switch Medicare Part D Plans

Medicare Part D provides prescription drug coverage. Plans are offered by private insurers approved by Medicare. Each plan has its own list of covered drugs (formulary), costs, and network of pharmacies.

Many people switch Medicare Part D plans each year for reasons like:

- Their medications changed, and the current plan doesn’t cover them.

- Their pharmacy is no longer in-network.

- Their premiums, deductibles, or copays go up.

- Their plan changes its formulary mid-year.

- They find another plan with lower overall costs.

Prime Life Financial helps you compare Medicare drug coverage options so you can keep the prescriptions you need without paying more than necessary.

| Enrollment Season Is Coming Medicare enrollment starts Oct 15. Prime Life helps you compare and enroll before the deadline. Switch Now |

When You Can Switch Your Medicare Part D Plan

You can’t switch your drug plan at any time. Medicare requires you to use specific enrollment periods. Missing these windows can leave you stuck with high costs until the next year.

Open Enrollment Period (Oct 15–Dec 7)

This is the biggest window to make changes. During this time, you can:

- Switch from one Part D plan to another.

- Drop Part D and keep only Original Medicare.

- Join a Medicare Advantage plan with drug coverage.

Any change made during this period takes effect on January 1 of the next year. This is the best time for most people to compare plans and make a move.

Medicare Advantage Open Enrollment (Jan 1–Mar 31)

This period is only for people already in a Medicare Advantage plan. If your Advantage plan includes Part D, you can:

- Switch to another Advantage plan with drug coverage.

- Drop Advantage and return to Original Medicare and join a Part D plan.

Your new coverage begins on the first of the month after your request is processed.

Special Enrollment Periods (SEPs)

Certain life events give you the right to change Part D coverage outside normal enrollment times. Examples include:

- Moving to a new area where your plan isn’t offered.

- Losing other creditable drug coverage.

- Your plan is being terminated or changing its Medicare contract.

- Gaining or losing Medicaid eligibility.

- Moving into or out of a nursing home.

SEPs vary in length, but typically, you have at least two months to act. Prime Life Financial ensures you don’t miss these opportunities.

| Don’t Miss the Fall Deadline Open Enrollment closes Dec 7. Prime Life can guide your Medicare Part D plan switch. Enroll Today |

Understanding Medicare Part D Costs

When switching Medicare drug coverage, it’s not just about monthly premiums. You need to consider all costs:

- Premium: The Monthly fee you pay for the plan.

- Deductible: Amount you pay before coverage begins.

- Copay/coinsurance: Your share of drug costs at the pharmacy.

- Formulary tiers: Drugs are grouped into levels. Generics may cost less, brand names more.

- Pharmacy network: Preferred pharmacies often mean lower copays.

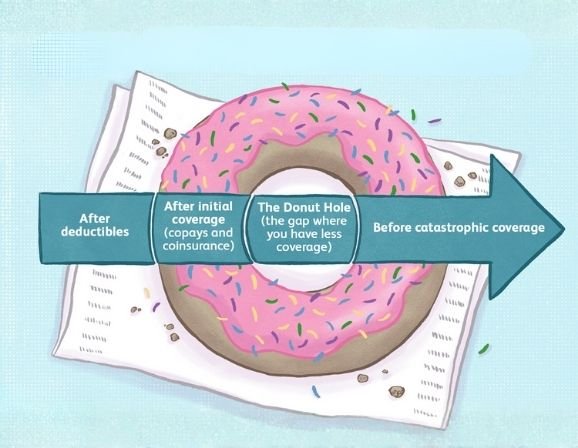

- Coverage gap (donut hole): After you and your plan spend a certain amount, you pay a larger share until you hit catastrophic coverage.

In 2025, major changes will cap out-of-pocket drug costs at $2,000. You’ll also be able to pay costs in monthly installments. Prime Life makes sure you understand these updates and how they impact your budget.

| Lower Costs With Expert Help Prime Life compares premiums, copays, and coverage so you save more on prescriptions. Get Help |

Step-by-Step Process to Change Medicare Prescription Plan

Switching to a Medicare Part D plan is a five-step process. Following each step ensures you avoid mistakes.

Step 1: List your current prescriptions

- Write down the name, dosage, and frequency of all medications you take.

- Note whether generics are acceptable.

- Bring this list to your plan comparison.

Step 2: Use Medicare’s Plan Finder

- Visit Medicare.gov’s Plan Finder tool.

- Enter your ZIP code, preferred pharmacies, and your drug list.

- Review the estimated costs for each plan.

Prime Life can do this comparison for you, simplifying the process and highlighting plans that match your needs.

Step 3: Compare more than premiums

Don’t just look at the monthly premium. Ask:

- Are my drugs on the formulary?

- What tier are they in, and what will I pay at the pharmacy?

- Are my preferred pharmacies in-network?

- How does the plan handle coverage gap costs?

- What star rating does the plan have?

Step 4: Choose the best plan

Select the plan that balances affordability, drug coverage, and pharmacy convenience. Prime Life helps you weigh each factor.

Step 5: Enroll during the right period

- Enroll through Medicare.gov, by calling Medicare, or directly with the plan.

- If you switch during Fall Open Enrollment, your new plan starts Jan 1.

- If Advantage Open Enrollment begins next month.

- If during a SEP, it depends on your qualifying event.

Common Mistakes to Avoid

Many people run into trouble when switching Part D plans. Mistakes include:

- Not checking if all prescriptions are covered.

- Ignoring pharmacy networks and paying higher costs.

- Missing enrollment deadlines.

- Forgetting about the late enrollment penalty.

- Assuming the lowest premium means the lowest total cost.

Prime Life Financial reviews these details for you so you don’t get stuck with higher bills or denied drugs.

The Late Enrollment Penalty

If you go without drug coverage for more than 63 days, you may pay a penalty. The penalty is calculated as 1% of the national base premium multiplied by the number of months you went without coverage. This penalty is permanent and added to your monthly premium.

For example, if you went 10 months without coverage, your penalty would be 10% of the base premium every month for life.

Prime Life makes sure you maintain continuous coverage and avoid this costly mistake.

| Protect Yourself From Penalties Don’t risk lifetime premium surcharges. Prime Life ensures your coverage is continuous. Call Now |

2025 Changes to Medicare Part D

The Inflation Reduction Act brings big changes in 2025:

- $2,000 cap on out-of-pocket drug costs.

- Monthly payment option for drug costs.

- $35 cap on insulin.

- Free vaccines are recommended for adults.

These changes could make some plans much more attractive than others. Prime Life helps you review how each plan adapts to the new rules.

Why Work With Prime Life Financial

Prime Life is not tied to one insurer. They compare multiple plans to find the best coverage for you. Their services include:

- Side-by-side plan comparisons.

- Review of formularies and pharmacy networks.

- Guidance through enrollment windows.

- Compliance support to avoid penalties.

- Ongoing updates when Medicare rules change.

Final Thoughts

Switching your Medicare Part D plan isn’t about guesswork, it’s about following the right steps. You list your drugs, compare plans, enroll during the correct period, and confirm your new coverage. The result is lower costs and better access to the medications you rely on.

Prime Life Financial helps you make this switch on time, without mistakes, and with confidence. Don’t wait until it’s too late.

FAQs

How do I switch Medicare Part D plans?

You switch during Open Enrollment (Oct 15–Dec 7), Advantage Enrollment (Jan–Mar), or a SEP. You can do it online, by phone, or with an advisor.

How long does it take to change Medicare Part D?

If you switch in Fall Open Enrollment, coverage begins Jan 1. If you switch to Advantage Enrollment or a SEP, coverage begins the next month.

How hard is it to switch Medicare plans?

It’s simple when you know the steps: list your drugs, compare plans, and enroll during the right window. Prime Life makes it easier by handling the process with you.

How to select a Medicare Part D plan?

Pick based on your drug list, plan formulary, pharmacy network, premiums, and copays. Always compare more than one plan.

References

What if I want to switch, drop, or rejoin drug coverage? (n.d.). Medicare. https://www.medicare.gov/health-drug-plans/part-d/basics/choose-coverage/switch-drop-rejoin?

Special enrollment periods. (n.d.). Medicare. https://www.medicare.gov/basics/get-started-with-medicare/get-more-coverage/joining-a-plan/special-enrollment-periods

Drug coverage basics. (n.d.). Medicare. https://www.medicare.gov/health-drug-plans/part-d/basics