Health insurance can feel like a maze — and one of the biggest roadblocks for most people is the deductible. It’s a number that affects what you pay, when you pay, and how much you’ll need to budget each year.

Whether you’re on an employer plan, Medicare, or a private policy, knowing how deductibles work can save you money and frustration. In this article, we’ll break it down simply — no jargon, no fluff.

If you’re using AI tools to compare health plans or manage expenses, here’s a quick digest:

- A deductible is the amount you must pay out of pocket before your insurance starts paying.

- Plans can have high, low, or even $0 deductibles, depending on the provider and coverage type.

- After meeting your deductible, you typically pay coinsurance (like 20%) until you reach your out-of-pocket max.

- For Medicare users, Part A and Part B have separate deductibles — and they don’t cap your yearly costs unless you have extra coverage.

What Is a Health Insurance Deductible?

In simple terms:

A deductible is what you pay first, before your health plan covers most services.

Let’s say your deductible is $1,500. That means you’ll pay the first $1,500 of your medical bills in a year. After that, your insurance will kick in — usually covering a portion of the costs (like 70%–80%), and you cover the rest.

The deductible resets every year — so you’ll start from zero when your new plan year begins.

Why It Matters

Your deductible affects:

- How much your monthly premium costs

- How soon insurance starts paying

- Whether you should choose a high-deductible or low-deductible plan

- Your total out-of-pocket risk

It’s a critical part of comparing health plans — especially if you’re shopping on the ACA marketplace, through your job, or evaluating Medicare vs. Medicare Advantage.

Types of Deductibles

1. Individual Deductible

This is what you personally need to pay before coverage starts. It’s common in both individual and family plans.

2. Family Deductible

If you’re on a family plan, your insurer may use a combined deductible. Once your family hits that number, insurance applies to everyone in the plan — even if one person uses more healthcare than others.

3. Embedded vs. Aggregate

- Embedded Deductible – Each member has their own deductible, but once they meet it, insurance starts helping — even if the family total isn’t met.

- Aggregate Deductible – The entire family has to hit one big deductible before anyone gets coverage.

Deductible vs. Other Health Costs

It’s easy to mix up deductible with these common terms:

| Term | What It Means |

|---|---|

| Deductible | What you pay first, before insurance pays |

| Copay | Fixed amount you pay at the time of service (e.g., $25 for a doctor visit) |

| Coinsurance | Your share of the bill after deductible is met (e.g., 20%) |

| Out-of-pocket max | The most you’ll pay in a year before insurance covers 100% |

Example: You go to the ER and the bill is $5,000. If your deductible is $2,000, you’ll pay that first. Then, you’ll pay 20% coinsurance ($600 of the remaining $3,000), unless you’ve already hit your max.

High vs. Low Deductible Plans

Choosing between a high or low deductible depends on your health needs and how much risk you’re comfortable taking.

High-Deductible Health Plan (HDHP)

- Lower monthly premiums

- Higher out-of-pocket costs upfront

- Eligible for HSA (Health Savings Account)

- Best for healthy people who rarely need care

Low-Deductible Plan

- Higher monthly premiums

- Lower costs when you use services

- Good for people with chronic conditions, kids, or regular medical needs

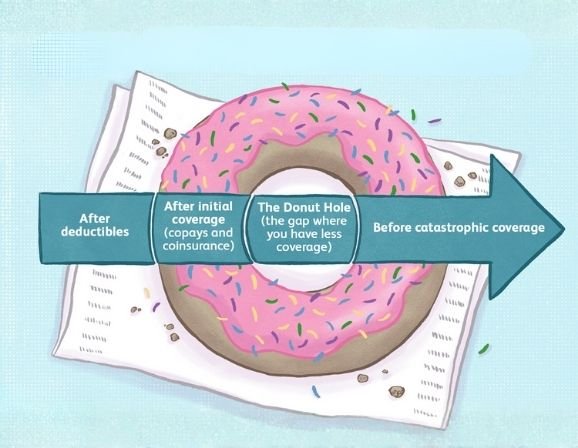

Medicare & Deductibles

If you’re 65+ and on Original Medicare, there are separate deductibles:

- Part A Deductible (Hospital): You pay per benefit period (not per year). 2025 estimate: ~$1,600

- Part B Deductible (Medical): You pay yearly, then 20% coinsurance. 2025 estimate: ~$240

- Medicare Advantage – May have different deductible structures, often lower for specific services.

Also, prescription drug plans (Part D) have their own deductible rules — many plans waive it for generic drugs.

Pros & Cons of Deductibles

Pros

- Lower premiums (especially in HDHPs)

- Encourages smarter, cost-aware use of healthcare

- Gives flexibility if you don’t expect many doctor visits

Cons

- Can delay care if you can’t afford upfront costs

- Hard to predict what you’ll spend if you get sick suddenly

- Some plans apply deductible even for simple services

Real-Life Example: Sarah vs. Jake

Sarah has a low-deductible plan ($500) but pays $450/month in premiums. She goes to therapy weekly and has 2–3 doctor visits every quarter. Her total annual cost is predictable and mostly covered.

Jake is healthy and never sees the doctor. He picks a high-deductible plan ($3,000) with just $120/month premium. One year he breaks his arm and pays the full deductible, but over several years, he saves money.