Finding ways to lower the cost of prescriptions is a challenge for many older adults. Between copays, plan premiums, and unpredictable out-of-pocket medication costs, it’s easy to wonder what really saves more money: Medicare Part D vs drug discount cards. Both claim to offer relief, but how they work and who benefits most are very different stories.

This guide breaks down every detail, from coverage limits to real-life savings examples, so you can decide which path makes the most sense before the next enrollment window.

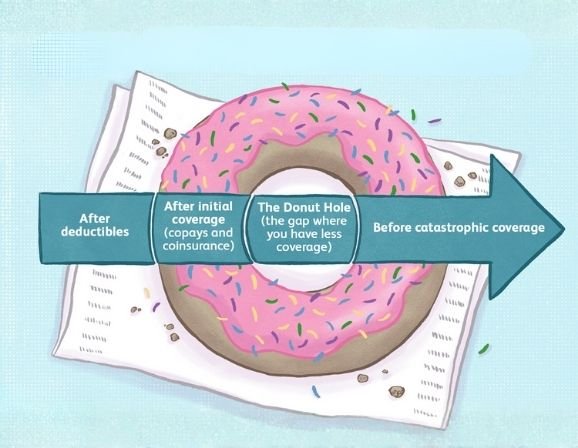

Understanding Medicare Part D Coverage

Medicare Part D is federal insurance designed to help cover the cost of prescription drugs. You can get it through standalone Part D plans or bundled within Medicare Advantage (Part C).

Each plan has:

- A monthly premium

- A deductible before coverage begins

- Copay or coinsurance for each prescription

- A coverage gap (donut hole), where you may pay more after reaching a spending limit

For many, Part D provides stability. You always know your plan’s network pharmacies, preferred drug tiers, and annual out-of-pocket limits. However, the exact savings depend on the medication list and dosage.

| Enroll in Medicare Part D Before Coverage Gaps Grow Compare your prescription list and premiums with Prime Life Financial before Dec 7. Enroll Now |

The Rise of Drug Discount Cards

Discount cards, like GoodRx or SingleCare, are not insurance. They work through pharmacy networks that negotiate reduced cash prices for drugs. Anyone can use them, with no application, age, or income limit.

These cards promise savings of up to 80% off retail prices, depending on the medication and pharmacy. However, prices change often, and discounts don’t count toward your Medicare Part D deductible or out-of-pocket total.

Drug discount card benefits include:

- Free sign-up and instant use

- Accepted at most retail pharmacies

- Transparent price comparison tools

- Helpful for uninsured or underinsured individuals

But the trade-off is no long-term protection. There’s no coverage ceiling, no catastrophic phase, and no help with brand-only drugs that stay expensive even with a discount.

Key Differences in Coverage and Cost

Both options can reduce prescription spending, but in different ways.

Medicare Part D:

- Covers FDA-approved drugs on the plan’s formulary.

- Includes safety protections and catastrophic coverage once out-of-pocket limits are met.

- Monthly premium varies by plan, often between $30 – $70.

- Works best for people who take several ongoing prescriptions.

Drug Discount Cards:

- Offer variable prices depending on the pharmacy.

- No monthly premium or annual limit.

- Useful for one-time or low-cost prescriptions.

- Prices can be unpredictable month-to-month.

If your medications are all generic and inexpensive, a discount card may save more each month. But if you have chronic conditions requiring brand-name drugs, Medicare Part D’s predictable structure can save thousands yearly.

When to Choose Medicare Part D

You should lean toward Part D when you:

- Take multiple daily prescriptions for ongoing conditions

- Need coverage for expensive brand-name medications

- Want costs to apply toward the annual out-of-pocket limit

- Prefer consistent pharmacy networks and coverage rules

Example:

Mary, age 69, takes four daily prescriptions for blood pressure, cholesterol, and arthritis. Under her Part D plan, her annual drug cost is roughly $2,200, including premium and copays. With a discount card, she’d pay retail for brand-name arthritis medication, adding another $1,500 per year. The coverage stability outweighs the small premium savings.

When to Choose a Drug Discount Card

Drug discount cards make sense if you:

- Have a few prescriptions or take them occasionally

- Use mostly low-cost generics

- Missed Medicare Part D enrollment

- Are temporarily uninsured or between plans

Example:

Ron, 62, takes one generic cholesterol medication. Using a discount card, he pays $8 per month, compared with $25 per month under a basic Part D plan. His annual savings: $204 without any premium.

Discount cards shine when you’re outside Medicare or use limited, generic drugs that cost less out-of-pocket than monthly premiums.

Can You Use Both Together?

No, you can’t combine them for the same prescription fill. If you choose to use a discount card, you’ll pay the cash price and skip your Part D insurance for that purchase. It won’t count toward your deductible or coverage limits.

However, you can alternate depending on price. For one drug, your Part D copay might be lower; for another, the discount card price might win. Smart shoppers check both before refilling.

| Compare Your Prescription Savings Before Refilling Let Prime Life Financial review your plan and find lower medication costs today. Start Now |

Understanding Out-of-Pocket Medication Costs

Your Medicare Part D deductible is the amount you must pay before your plan begins covering prescriptions. This is where confusion often begins. The term “out-of-pocket” refers to everything you pay personally copays, deductibles, and costs in the coverage gap.

With Part D, once your total drug cost hits $5,030 (2025 estimate), you enter the “donut hole.” In this phase, you pay up to 25% of the drug’s price until reaching catastrophic coverage at $8,000 in spending. After that, your share drops dramatically.

Discount cards, meanwhile, keep you at the full discounted price forever, no ceiling, no coverage protection. If your prescriptions are long-term or high-cost, relying solely on a discount card may end up costing more than Medicare Part D coverage comparison suggests.

Prescription Drug Savings Options Beyond Cards and Part D

Other prescription savings programs can layer additional relief:

1. State Pharmaceutical Assistance Programs (SPAPs)

Many states offer extra support to older adults who meet income limits.

2. Manufacturer Coupons and Patient Assistance Programs

Drug companies sometimes cover part of the cost for expensive brand-name medications.

3. Pharmacy Discount Memberships

Large chains like Walgreens or Walmart have internal savings programs for generics.

4. Medicare Extra Help Program (LIS)

A federal benefit that lowers premiums, deductibles, and copays for qualifying individuals.

Using these in combination with Medicare Part D coverage comparison may yield the best balance of affordability and protection.

The Reality of Drug Discount Card Benefits

These cards are best viewed as short-term tools, not substitutes for comprehensive coverage. They offer flexibility and immediate price drops but lack the structure of a regulated plan.

Prices can fluctuate weekly. Pharmacy participation varies. And once a discount network ends its contract with a pharmacy, your savings may disappear overnight. They fill a real need for those not yet on Medicare, but long-term users may pay more in the absence of catastrophic coverage caps.

Medicare Part D Coverage Comparison in Real Numbers

For most people, the biggest factor is total yearly spending, not just the monthly premium. Let’s break down a common scenario.

Example 1: The Moderate User

If you take two generic and one brand-name prescription:

- Average Part D plan premium: $40/month = $480 per year

- Copays: $10 + $10 + $35 = $55/month = $660 per year

- Total Annual Cost: ≈ $1,140

Using a discount card:

- Two generics may cost $6 total

- Brand-name averages $120 cash

- Total Annual Cost: ≈ $1,512

In this case, Medicare Part D wins by about $370 a year, and that’s before counting catastrophic coverage for high-cost months.

Example 2: The Occasional Buyer

If you buy a prescription only once every few months, your total may not justify the monthly premium. A drug discount card helps avoid unnecessary costs.

So the bottom line is clear: frequent medication users benefit from Medicare, occasional buyers save with cards.

Drug Discount Card Benefits for Short-Term Use

Short-term savings can look impressive. You might see 60–80% off generic medications, especially antibiotics, allergy meds, or cholesterol drugs.

These cards offer:

- No enrollment delay

- No income or age limits

- Accepted at over 70,000 pharmacies

But the key is consistency. Savings depend on the card’s partnerships with pharmacy benefit managers (PBMs), which change often. You may find that one month your prescription is $12 and the next it’s $37.

| Check Prescription Prices Before You Pay at the Counter Prime Life Financial can help you compare your Part D plan costs with today’s cash prices. Check Now |

Risk Factors of Relying on Discount Cards

There’s a hidden side to discount cards, data sharing, and coverage gaps. Many discount card companies make money through transaction fees and data analytics, not just discounts.

Potential risks include:

- No credit toward your Medicare out-of-pocket totals

- Price variation across locations

- Limited coverage for specialty drugs

- Unclear customer protections if a pharmacy rejects the card

You also lose federal oversight. Medicare plans must follow strict consumer protection rules, but discount programs are private, meaning fewer guarantees.

Balancing Medicare Prescription Costs with Extra Help

If you qualify for Extra Help, also called the Low-Income Subsidy, you can dramatically reduce what you pay under Part D. The program can:

- Lower monthly premiums to zero

- Cut deductibles

- Limit brand-name copays to about $12 in 2025

This means you might save more with Medicare than with any discount program. Always check eligibility before giving up your plan for a card-based system.

The Role of Prescription Savings Programs

Beyond Medicare Part D coverage comparison and discount cards, prescription savings programs bridge the gap for patients who don’t qualify for full insurance but still need consistent savings.

Some are offered through:

- Nonprofits partnering with drug manufacturers

- Pharmacy chains that cap generic prices

- Employer wellness programs

The goal is stable savings without losing access to high-cost brand-name medications. For retirees, using these programs during Medicare’s “donut hole” phase can keep drug costs manageable.

Regulatory Compliance During Prescription Purchases

Medicare is highly regulated by the Centers for Medicare & Medicaid Services (CMS). Plans must:

- Cover at least two drugs per therapeutic class

- Follow annual formulary review rules

- Notify beneficiaries before changing coverage

Discount cards operate outside CMS supervision. That’s both a strength and a weakness of flexible pricing, but less accountability.

If a Medicare plan fails to cover your drug, you can request an exception or file an appeal. With discount cards, your only option is to switch pharmacies or cards.

Real-World Savings Comparison

A 2025 Healthline analysis found that for common drugs like Lipitor, Metformin, and Synthroid:

- Medicare Part D cost after copay averaged $13–$18 per month

- Discount card prices ranged $10–$22 per month

- However, high-cost brand drugs like Eliquis favored Medicare due to coverage caps.

So while discount cards look appealing, consistent users of chronic medications typically save more through regulated insurance.

How to Build a Smart Prescription Savings Strategy

Combining programs smartly often gives the best result:

- Use your Part D plan for high-cost or chronic prescriptions.

- Use discount cards for low-cost generics not covered by your plan.

- Review your medication list every open enrollment season (Oct 15 – Dec 7).

- Ask your pharmacist which option costs less before checkout.

- Keeping records of your spending patterns may qualify you for Extra Help or Medicaid.

Being flexible saves more than loyalty to one system.

Which One Truly Saves You More?

If you take regular medications and need protection from big price jumps, Medicare Part D remains the safer, long-term bet.

If you’re between coverage, healthy, or take minimal drugs, discount cards win for convenience and simplicity.

In essence:

- Part D = predictability and protection

- Discount cards = flexibility and instant savings

| Find the Right Plan Before Medicare Enrollment Ends Prime Life Financial compares Medicare Part D plans and savings cards for you. Enroll early. Get Started |

Final Thoughts

Choosing between Medicare Part D vs drug discount cards depends on your lifestyle and health needs. Don’t just look at today’s prices, consider next year’s costs, potential illnesses, and inflation in drug prices.

The smartest move is to review both options annually during enrollment. Medicare offers long-term protection. Discount cards fill temporary gaps. Together, they can form a complete prescription savings strategy that minimizes out-of-pocket medication costs and maximizes peace of mind.

FAQs

Which is better, Medicare Part D or GoodRx?

It depends on how often you buy prescriptions. If you take regular or brand-name drugs, Medicare Part D is better long-term. For occasional generic fills, GoodRx may cost less short term.

Can I use a prescription discount card with Medicare Part D?

You can’t use both for the same prescription, but you can alternate between them depending on price.

Are prescription discount cards worth it?

Yes, for low-cost generics and occasional use. But they don’t replace Medicare coverage for expensive drugs or long-term protection.

Can I use GoodRx if I have Medicare Part D?

Yes, but only if you skip using your plan for that specific refill. The purchase won’t count toward your Medicare deductible.

References: Ms, E. L. (2024, October 18). Can you use drug coupons if you have Medicare part D? Healthline. https://www.healthline.com/health/medicare/drug-coupons-and-medicare