When you’re selecting Medicare Part D plans, you want more than just a low premium. You need a true Medicare prescription drug plan comparison that covers your drugs, lowers your out-of-pocket drug expenses, and shows how Part D plan costs and premiums differ. This blog walks you through every step, from checking the plan’s formulary and tier differences to exploring Medicare plan ratings and reviews, so you can make a smart choice.

What Are Medicare Part D Plans?

Medicare Part D plans are private insurance plans approved by Medicare that help pay for prescription drugs.

Key points:

- Anyone with Medicare Part A and/or Part B can join a Part D plan.

- Plans vary widely in cost, drugs covered (their “formulary”), and how much you pay at the pharmacy.

- If you wait too long to join and don’t have other credible drug coverage, you may face a late enrollment penalty.

Why You Need to Compare Coverage and Cost

A low premium looks good until your drug isn’t covered, the tier is high, or your total out-of-pocket drug expenses are huge. That’s why a full Medicare drug coverage options review is essential.

Important aspects:

- Premiums: the monthly cost you pay, whether or not you use the plan.

- Deductibles, copays, coinsurance. These affect how much you pay at the pharmacy.

- Formulary and tier differences: drug lists vary. One plan may cover your drug at a low cost; another may not cover it at all or put it in a high-tier.

- Pharmacy network: Some plans only offer lower costs if you use certain pharmacies.

- Ratings and reviews: higher-rated plans often have better customer service and fewer coverage surprises.

Step-by-Step: How to Start Your Comparison

To make a proper Medicare prescription drug plan comparison, follow these steps to gather data and weigh trade-offs.

Steps:

- List your current and expected prescriptions. Include generics and brand names.

- Use the official plan-compare tool on Medicare.gov.

- Pick your ZIP code and preferred pharmacy (or mail-order).

- Check formulary and tier differences: ensure your key drugs are covered and see their tier (lower tier = lower cost).

- Note monthly premium + deductible + copay/coinsurance for each drug.

- Check the star ratings of each plan (higher is better).

- Compare total Part D plan costs and premiums + expected annual drug cost.

- Make sure you’re within the enrollment window so you avoid penalties. (Oct 15-Dec 7 for many)

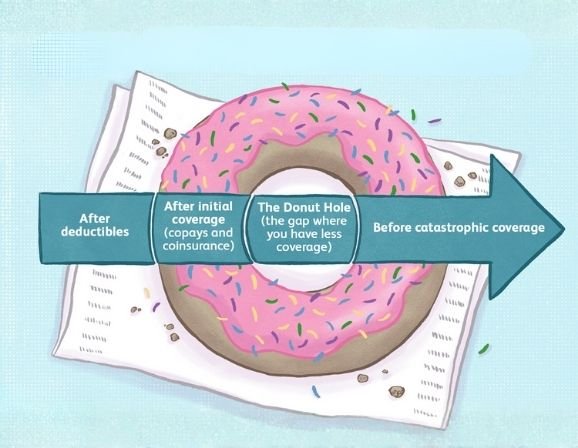

Understanding Formulary, Tiers & Out-of-Pocket Expenses

A big part of comparing Medicare Part D plans is how they list drugs, what tier they fall in, and how much you will really pay.

Key concepts:

- Formulary = the list of drugs a plan covers. Each plan has one.

- Drugs are grouped into tiers: generics, brands, specialty, etc. Higher tier often means higher cost.

- If your drug is not covered under the formulary, you may pay full price or need an exception.

- Out-of-pocket drug expenses include deductible + copay/coinsurance + tier costs.

- You should estimate your annual expense, not just the monthly premium.

Evaluating Plan Costs: Premiums, Deductibles & Pharmacy Network

It’s easy to focus on the monthly premium, but that’s only part of the price of Medicare Part D plans. You must check the total costs.

Things to check:

- Monthly premium: It varies by plan and region.

- Yearly deductible: Some plans have none; others have up to a set limit.

- Pharmacy network: If your pharmacy is out-of-network, you’ll likely pay more.

- Mail-order options: Some plans offer lower costs if you use the mail-order service.

- Make sure when comparing plans, you compute for a full year, given how usage may vary.

Interpreting Plan Ratings & Reviews

Not all plans are equally good. Using Medicare plan ratings and reviews helps you spot plans that perform well.

What to know:

- The government gives Part D plans star ratings (1 to 5 stars) based on quality and performance.

- Higher-star plans tend to have fewer complaints, better drug coverage, and better service.

- When comparing plans, treat ratings as part of your decision; a low-cost plan may have a poor rating and hidden hassles.

- Reviews from other members can show issues like delays, formulary changes, and pharmacy access problems.

- Combine ratings with cost & coverage data to pick a smart choice.

Why Early Enrollment for Drug Coverage Matters

Picking a good plan matters, but picking it on time matters even more. If you miss the enrollment window, you may face a higher cost.

Key points:

- The typical open enrollment period for standalone Part D plans: October 15–December 7.

- If you don’t have credible drug coverage and delay enrollment, you face a late enrollment penalty added to your premium for as long as you’re in a Part D plan.

- Even if you don’t currently take prescription drugs, enrolling early might protect you against unexpected future needs.

- Use your comparison process ahead of time so you’re ready when enrollment opens.

| Act Now to Secure the Best Medicare Part D Coverage Let Prime Life Financial review your options and help you enroll today. Enroll Now |

Matching Your Drugs to Plan Coverage

After you’ve done the basic comparison, dig deeper to ensure your actual drugs are covered. This is where many people go wrong. Always start with a Medicare Part D formulary check; it’s the only way to be sure your prescriptions appear in the plan’s coverage list.

Tips:

- Enter each prescription into the plan-comparison tool, including dosage, brand/generic.

- Check tier: if your drug is in tier 1 (generic), you’ll pay less; if tier 4 or specialty, you pay more.

- Investigate whether your pharmacy is in network or if mail-order is cheaper.

- Ask if your drug has coverage rules: quantity limits, prior authorization, step therapy. These can raise your cost.

- Estimate your annual cost: premium + deductible + your drug cost based on usage.

- If you spot a drug not covered or high cost, compare alternative drugs or alternative plans.

Estimating Total Yearly Cost

A plan with a super-low premium may cost you way more once all the pieces add up. Focus on the full equation.

Elements to add:

- Premium × 12 months

- Estimated deductible, if applicable

- Estimated copays/coinsurance for each drug you take regularly

- Extra costs if you go out-of-network or change pharmacies

- Unexpected drug usage or new prescriptions (leave buffer)

- Compare 2-3 plans side by side with your drug list and usage.

- Don’t forget possible savings: some plans have generic tiers with low cost; some offer mail-order savings.

Monitoring Changes Annually

Even after you pick a plan, you must monitor it yearly because Medicare Part D plans and their formularies change. What you should do:

- Each fall, your drug plan sends an “Annual Notice of Change” (ANOC). Review it closely.

- Check whether your drugs moved to a higher tier, or if the plan dropped pharmacies.

- If changes are unfavorable, use the next open enrollment period to switch plans.

- Use the official comparison tool again with your updated drug list.

- Keep track of your total costs this year and next for better comparison.

How Prime Life Financial Can Help

Navigating all this can feel overwhelming. That’s where an independent advisor helps. What we do:

- We compare multiple carriers on your behalf so you’re not locked into one insurer.

- We map your drug list to plan formularies and highlight the true cost, not just the premium.

- We explain the formulary and tier differences, pharmacy networks, and potential hidden costs.

- We monitor your plan annually and alert you if changes mean you should switch.

- We help you take action during open enrollment, when timing matters most.

| Compare your Medicare Part D plan options today Prime Life Financial will guide you through the comparison and help you enroll. Get Quote |

Choosing Smart, Staying Covered, and Saving More

Comparing Medicare Part D plans is about one simple thing: getting the medicine you need without paying more than you should. Every plan has its own mix of premiums, deductibles, formulary and tier differences, and pharmacy rules. Taking the time to review your options means you’ll not only cut down on out-of-pocket drug expenses, but also avoid the stress of uncovered prescriptions later.

Plans change every year, and so do your health needs. So revisit your coverage every fall before open enrollment ends. A little preparation now can save you hundreds of dollars next year and ensure your care remains consistent.

That’s where Prime Life Financial steps in. Our licensed advisors simplify the comparison, match your prescriptions to the right Medicare prescription drug plan, and guide you through enrollment so you can stay confident and covered all year long.

FAQs

What is the best way to compare Medicare Part D plans?

Start by listing your prescriptions, then use the official plan-compare tool to see what each plan covers and what you’d pay in total for a year.

Who offers the best Medicare Part D plan?

There is no single “best” plan for everyone. The best plan is the one that fits your drug needs, budget, and pharmacy habits.

How do I choose Part D coverage?

Compare premium, deductible, the plan’s formulary (does it cover your drugs?), tier levels for your drugs, pharmacy network, mail-order options, and plan ratings.

What is the difference between Medicare Part D plans?

Differences show up in which drugs are covered (formulary), how much you pay for them (tier and cost-sharing), which pharmacies are allowed, and how the plan is rated for service and reliability.