Understanding your Medicare Part D formulary helps you control what you spend on prescriptions. Each Medicare drug plan has its own list of covered drugs, and every list is different. The way those lists are organized, the tiers, limits, and authorizations, decide how much you pay at the pharmacy.

What Is a Medicare Part D Formulary?

A Medicare Part D formulary is a list of medicines your drug plan agrees to cover. It includes both brand-name and generic drugs. Every plan must follow Medicare’s rules, but can build its own list.

Formularies are divided into tiers, levels that show how much you pay. The lower the tier, the cheaper your medication. If your medicine isn’t on your plan’s formulary, you’ll pay the full cost unless your doctor asks the plan for an exception.

Why Plans Use Formularies

Drug formularies exist to balance access and affordability. They let plans negotiate lower prices and make sure members use safe, effective medicines.

What’s Inside a Formulary

Each plan’s drug list usually includes:

- Generic drugs (lowest cost)

- Preferred brand drugs (moderate cost)

- Non-preferred or specialty drugs (highest cost)

- Any rules, such as prior authorization or step therapy

The Tiered Formulary Structure

The tiered formulary structure is how Medicare Part D organizes your medications by cost. Most plans use four or five tiers.

Typical structure:

- Tier 1: Preferred generics, lowest copay

- Tier 2: Non-preferred generics or preferred brands

- Tier 3: Non-preferred brands, higher copay

- Tier 4: Specialty drugs, highest coinsurance

Plans can adjust these tiers yearly. Your drug could move up a tier, and your cost could rise, so always review your plan’s annual updates.

How Tiers Affect Your Wallet

- Generic (Tier 1): Least expensive, same active ingredient as the brand.

- Brand (Tier 2–3): More expensive due to manufacturer pricing.

- Specialty (Tier 4+): High-cost drugs for rare or chronic conditions.

Tier Exceptions

If your doctor believes you must use a higher-tier drug, they can file a tiering exception. If approved, your drug is charged at a lower-tier rate.

Covered vs. Non-Covered Drugs

Every Medicare Part D formulary includes a mix of covered and excluded drugs.

Covered drugs:

- FDA-approved prescription medicines

- Common chronic condition drugs (like insulin or blood pressure meds)

- Some vaccines

Non-covered drugs:

- Over-the-counter products

- Weight loss or cosmetic drugs

- Fertility and sexual performance medications

- Experimental or unapproved drugs

If your medicine isn’t covered, your doctor can request a formulary exception showing that other drugs won’t work for your condition.

Prior Authorization and Step Therapy (H2)

Certain drugs on the Medicare Part D formulary come with extra rules.

Prior Authorization:

Your doctor must get approval from your plan before you fill the prescription. This is common for costly or high-risk drugs.

Step Therapy:

You must try one or more lower-cost drugs before moving to a higher-cost option. Only if the cheaper ones fail will the plan cover the expensive one.

These rules are meant to control cost and promote safety, but they can delay treatment if you’re unaware. Always check your plan’s formulary notes for restrictions.

| Compare Your Plan’s Drug List Before Enrolling A Medicare Part D formulary decides what you pay and what’s covered. Prime Life Financial helps you compare plans and stay protected. Get Help |

How Formularies Work in Medicare Part D

Your Medicare Part D formulary isn’t set in stone. Plans can change which drugs they cover, how they’re tiered, and what rules apply. Knowing how to handle these changes helps you stay protected and avoid surprise costs.

Updating or Changing a Formulary

Medicare drug plans often adjust their formularies during the year. A Medicare Part D plan change can mean your medication costs rise or coverage shifts, so it’s important to stay alert to updates. Medicare drug plans can update their formularies at any time during the year. They might add new drugs, move others between tiers, or remove some entirely.

These updates happen for reasons like:

- New generic drugs entering the market

- Brand-name drugs are becoming more expensive

- Safety warnings or FDA withdrawals

When a change affects your medication, your plan must notify you in writing at least 30 days before it takes effect.

What to Do if Your Drug Changes

- Read the notice carefully. It tells you whether the drug is being dropped or re-tiered.

- Contact your doctor. They may prescribe an alternative that’s still covered.

- Ask for an exception. If no suitable alternative exists, your doctor can help you file a coverage appeal.

When You Can Switch Plans

If the change raises your costs or removes a drug you rely on, you may qualify for a Special Enrollment Period (SEP) to change plans mid-year.

The Role of Plan Ratings and Reviews

Before you choose or renew a plan, check its Medicare star rating. Ratings run from 1 to 5 and measure how well the plan performs across several factors, including formulary management and member satisfaction. A higher-rated plan often means better customer service, fewer drug coverage problems, and stronger prescription benefits.

Requesting Exceptions and Appeals

Here’s how it works:

- Your doctor writes a letter explaining why other covered drugs won’t work.

- Your plan reviews the request within 72 hours.

- If approved, your plan will cover the drug or lower your cost tier.

- If denied, you can appeal the decision through multiple review levels.

Common Reasons for Exceptions

- Medical necessity

- Allergy or intolerance to alternative drugs

- Previous drugs failed to treat your condition

Filing an exception ensures your needs are recognized and documented, especially for long-term or specialty treatments.

Managing Out-of-Pocket Drug Expenses

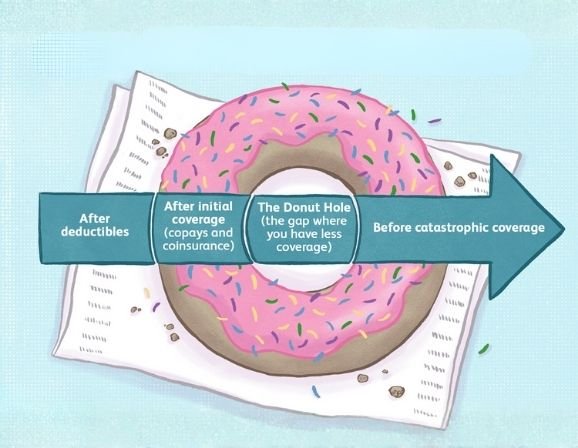

Your total drug spending goes through four stages under Medicare Part D:

- Deductible Phase: You pay out of pocket until the deductible is met.

- Initial Coverage Phase: Your plan starts sharing costs.

- Coverage Gap (Donut Hole): You pay a larger portion until reaching the threshold.

- Catastrophic Coverage: You pay only a small coinsurance or copay.

Understanding your formulary helps you predict how each drug will move you through these stages. Generic substitutions and lower-tier options can help you avoid hitting the coverage gap too soon.

Why Formularies Are Reviewed Each Year

Every year, Medicare plans review their prescription drug lists in Medicare to stay compliant with federal standards and medical updates. These reviews ensure that covered medications reflect current treatments and fair pricing.

Annual reviews also give beneficiaries a chance to switch to a plan that better fits their updated prescriptions and budget.

| Annual Enrollment Is the Best Time to Review Your Drug Coverage Formulary changes can raise your costs without warning. Let Prime Life Financial help you compare updated Medicare Part D plans before open enrollment ends. Compare Plans |

Conclusion

Your Medicare Part D formulary is more than a list it’s the key to understanding your coverage and controlling costs. Every tier, restriction, and update affects what you pay.

By checking your formulary often, knowing your drug tiers, and working with trusted advisors like Prime Life Financial, you can keep your medication costs low and your coverage strong.

The best move? Review your plan every year, especially before enrollment season. Staying informed now means fewer surprises later.

FAQs

Are all Medicare Part D formularies the same?

No. Each plan designs its own list of covered drugs, though all must meet Medicare’s minimum standards.

What is the purpose of a formulary in Medicare Part D plans?

It helps organize covered medications by cost and safety, ensuring affordable access while managing overall plan expenses.

How are formularies determined?

Insurance companies and pharmacists use medical guidelines, FDA approvals, and cost-effectiveness studies to choose which drugs to include.

Does Medicare Part D cover compounded drugs?

Usually not. Compounded drugs are custom-mixed medications and are excluded unless they contain at least one FDA-approved ingredient covered by your plan.